5 Ways To Reduce Your Money Stress

5 minute read

Over the last couple of decades, we’ve come to understand that health and wealth are inextricably linked. If you’re not healthy, it’s eventually going to wreak havoc with your finances. And if you’re not financially strong, it can be tough to afford the care you need to stay healthy.

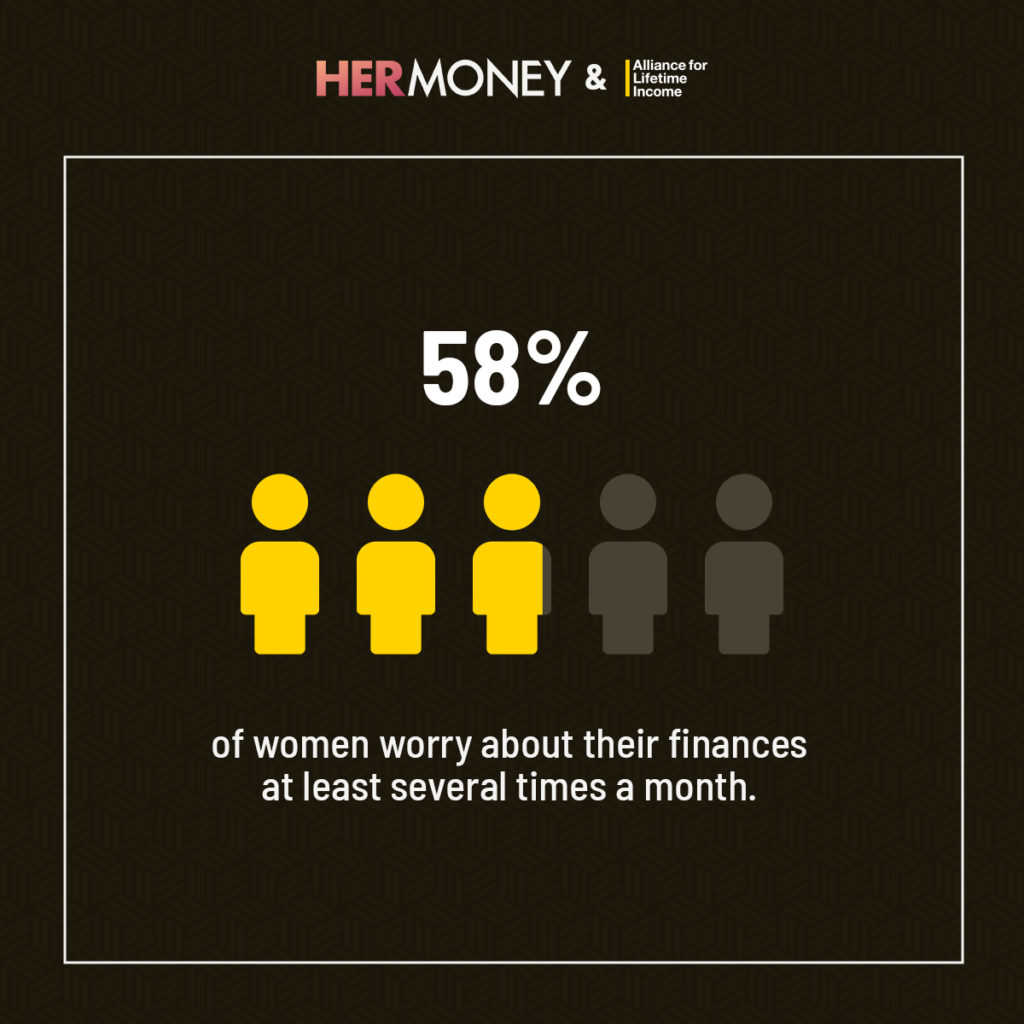

But when it comes to wealth and mental health? It’s taken us longer to make the connection. Only since the Great Recession – with some amplification from the coronavirus pandemic – have we really started to appreciate and try to quantify how much emotion and stress relate to money. The impact is substantial. According to The State of Women 2022, a study from HerMoney and The Alliance for Lifetime Income, nearly three out of five women (58%) worry about their finances at least several times a month, 28% worry several times a week and 14% worry every day. Only 10% of women say they have complete control over their financial stress. And when it comes to saving for retirement, the research shows more than half of women rank worrying about running out of money as one of their top two concerns.

It’s a beast that’s worth taming, says financial therapist Amanda Clayman. “Money and mental health intersect in some very unique and dynamic ways,” she notes. “People [really need to] embrace the idea of money holistically. And not only look at dollars and cents, but also think about the emotional and relational and cognitive and especially behavioral aspects of our financial health.”

Easier said than done? Perhaps. But if you find yourself feeling stressed out about your finances, here are five strategic ways to figure out exactly what’s behind your issues and find some relief. These insights are from Clayman’s recent appearance on Your Money Map, hosted by Alliance Education Fellow and HerMoney CEO Jean Chatzky.

WATCH Your Money Map: 5 Ways To Reduce Your Money Stress

On May 17, Your Money Map aired a pre-recorded episode with Amanda Clayman, a licensed clinical social worker and financial therapist who helps her clients understand how their thoughts, feelings, and past experiences shape their financial choices using Cognitive Behavioral Therapy, or CBT. She coaches people one-on-one, builds financial wellness programs for companies, and develops online courses on financial wellness on LinkedIn. Her work has been featured on CNBC, The New York Times, The Wall Street Journal, Forbes, and HerMoney.

The episode was titled, The Emotional Side of Retirement. Attaining financial stability and happiness in retirement is about more than just a dollar figure. It requires digging deep into your emotions around your money and your future: How do you feel about retirement? Are you worried about finding purpose? Are you scared of running out of money? And are you and your family on the same page? Jean Chatzky and Amanda Clayman discussed the answer to all these questions and more about our financial wants, needs, and fears in retirement.

Think Back – Way Back

Many of the money behaviors you’re likely carrying around today have less to do with what you’ve learned about finances as an adult and more to do with the money attitudes you observed growing up. It was this realization that drew Clayman to the field of financial therapy. In her 20s, she dug herself into a credit card hole. When she started to try to work on the problem, the traditional financial methodology wasn’t doing it.

“The idea of getting out of the debt brought up all this shame for me,” she says. “And I realized I was carrying a lot of my parents’ anxiety around money. That was typical of the home I grew up in. And the process of getting out of that debt was not so much about having the right financial plan. It was really more about how to understand my triggers…and how to understand what happened to me where I felt like I couldn’t ask for help.”

It was an aha moment for her. To begin to find your own, ask yourself some pointed questions: What’s your first money memory? What was the general feeling about money in the home where you grew up? Once you understand the attitudes that have been with you for decades, you can start to formulate a plan to deal with them.

Consider What You May Be Hiding From Your Spouse (Or Financial Advisor)

Another way to isolate the financial issues that are plaguing you is to get honest about what you’re hiding from others. Shame and avoidance are big drivers of financial stress, Clayman notes. “We may feel as if we’re falling short of our own expectations of ourselves or what others may expect us to do in those situations,” she says.

If you’re able to talk to others about those experiences – to unpack them with a spouse or partner, or bring them to a financial advisor and work on a path to solutions – that’s great. But if you can’t talk about, for example, the debt you’re carrying or your inability to stop spending impulsively? That might call for a financial therapy session or two.

“I encourage my clients to bring me the mess,” Clayman says. “And together we work out what is really causing the stress in their lives. [We get into] when it’s really not about the money, it’s just about what the money represents…and bring some clarity so that people aren’t stuck in those feelings of shame and avoidance.”

Understand The Shame

And while we’re on the subject of shame, it’s important to understand that the feeling isn’t always something to push away. Shame has a purpose. “It helps us make sense of things that we do that somehow may be threatening to our sense of belonging either in our family or, originally, in our tribe,” Clayman says. If we don’t have that sense of really belonging, it can be a matter of survival. In that way, shame is there to keep us safe. And that makes it a very strong motivator to do something, to take action to fix an underlying problem. So if you’re feeling shame about money, try not to turn it back toward yourself, she suggests. Instead of feeling like, “I’m a bad person,” focus on, “I’ve done a bad thing.” Then work on fixing the latter.

Separate Financial Stress From Emotional Stress

It’s basically impossible to avoid stress in our modern lives. That’s why Clayman urges trying to think of stressors along a continuum. Small stresses are what she calls “green light” stresses, where we feel like, although there are problems, we can mobilize our resources to meet them. Yellows are those that begin to bring on physical symptoms – tightness in your muscles, headaches, or digestive problems. And reds start to impact your thinking. In the latter two categories, she says, it becomes harder to differentiate between what’s truly a financial problem and what’s an emotional one.

The key is to formulate a plan to attack the problem (credit card debt, for example, or under-saving) by breaking it down into tasks. If you follow those tasks successfully and it still doesn’t reduce your symptoms, it’s likely got some emotional roots. “Then you need to look for emotional solutions,” she says. Seeking out support from a partner or friend, your HR department at work or a professional like a coach or therapist is the right next move.

Consider Financial Therapy

If financial therapy sounds like something you’d like to try, visit the website of the Financial Therapy Association. Use the “Find a FT” button locator to get connected with a practitioner who specializes in the issues you’re most concerned about. And note, Clayman explains, that this doesn’t have to be a lifetime engagement. She typically works with her clients for about a half dozen sessions – and then they move on with their lives.

For more resources on understanding and improving your relationship with money, as well as planning ahead so you can make your income last a lifetime, visit the Tools and Guides section of the Alliance website.